Offshore Company Formations vs Onshore Companies: Which Is Best for You?

Exactly How Offshore Business Formations Job: A Detailed Overview for Business Owners

Offshore company formations can supply considerable benefits for business owners seeking tax optimization and possession defense. The procedure entails several vital steps, beginning with careful territory choice and extensive paperwork preparation. Involving expert solutions is essential for compliance. Many forget the recurring responsibilities that adhere to initial enrollment. Recognizing these complexities can make a significant distinction in leveraging offshore opportunities successfully. The next steps are important for long-term success.

Comprehending Offshore Companies: What They Are and Why They Issue

Although the principle of overseas firms may seem complex, recognizing their essential nature and importance is necessary for both people and services seeking to optimize their economic techniques. Offshore business are entities registered outside the person's country of house, typically in territories that use beneficial governing atmospheres. These organizations can give various benefits, such as tax obligation optimization, possession protection, and improved personal privacy.

For entrepreneurs, developing an offshore business can facilitate worldwide profession, lower functional costs, and broaden market reach. In addition, overseas companies frequently permit streamlined conformity with international policies. People may additionally use offshore frameworks to safeguard personal possessions from political or economic instability in their home countries. Eventually, the charm of overseas companies copyrights on their capacity to enhance financial versatility and supply tactical advantages in a significantly interconnected global economic situation - Offshore Company Formations. Recognizing their functional structure and benefits is important for making notified decisions

Choosing the Right Jurisdiction for Your Offshore Business

Choosing the suitable territory for an overseas business is essential for maximizing tax benefits and guaranteeing compliance with regional guidelines. Various territories use differing tax obligation rewards and regulative atmospheres that can substantially influence service procedures. Subsequently, a careful assessment of these factors is vital for notified decision-making.

Tax Advantages Review

When taking into consideration the facility of an offshore company, recognizing the tax obligation advantages related to various territories is necessary. Various locations supply one-of-a-kind benefits, such as low or zero company tax obligation rates, which can significantly enhance productivity. Some jurisdictions give tax obligation motivations for details sorts of businesses, bring in entrepreneurs looking for minimized tax responsibilities. Furthermore, particular countries enforce positive tax treaties that minimize dual taxation on worldwide income, guaranteeing that organizations maintain even more incomes. The choice of territory also influences value-added tax (BARREL) and other neighborhood tax obligations. Entrepreneurs have to assess these aspects thoroughly to pick a location that straightens with their company objectives, enhancing tax obligation efficiency while staying certified with worldwide laws.

Regulatory Environment Considerations

Selecting the appropriate jurisdiction for an overseas firm requires a comprehensive understanding of the governing environment, as different countries enforce differing levels of compliance and administration. Business owners must assess aspects such as legal structures, tax obligation policies, and reporting responsibilities. Territories like the British Virgin Islands and Cayman Islands are commonly preferred for their business-friendly laws and minimal reporting needs. Alternatively, some nations might impose stringent guidelines that might make complex procedures and increase costs. Additionally, the political security and online reputation of a jurisdiction can impact the lasting feasibility of the offshore company. Consequently, careful factor to consider of these regulative facets is vital to ensure that the selected territory aligns with the company's tactical goals and operational demands.

Preparing the Required Documentation

Preparing the necessary documents is an important step in the offshore firm formation process. Business owners have to gather various lawful and identification documents to promote their business's establishment in an international jurisdiction. Generally, this includes a detailed service plan outlining the firm's goals and functional methods. Furthermore, individual identification records, such as copyright or vehicle driver's licenses, are required from the firm's directors and investors.

Oftentimes, proof of address, like utility bills or bank declarations, is necessary to verify the identities of the involved celebrations. Furthermore, particular types dictated by the territory, including application for registration, have to be finished properly. Some territories might likewise call for a declaration of the nature of service tasks and conformity with neighborhood policies. Extensively preparing these files ensures a smoother registration process and helps alleviate possible hold-ups or problems, eventually setting a strong foundation for the overseas entity.

Engaging Expert Providers for Offshore Formation

Involving specialist services in offshore formation can significantly boost the effectiveness and effectiveness of the process. Business owners often encounter intricacies that can be frustrating, making expert support very useful. Expert companies concentrating on overseas formations give a wealth of knowledge concerning jurisdiction selection, business framework, and regional market problems.

These experts can aid in composing important documentation, making sure precision and compliance with details needs. They also aid simplify interaction with local authorities, minimizing the probability of misconceptions or hold-ups. Additionally, expert solutions can offer understandings right into calculated benefits, such as tax obligation advantages and possession security, tailored to the business owner's particular requirements.

Navigating Regulatory Compliance and Legal Requirements

Comprehending the governing landscape is vital for business owners beginning on offshore company developments. Compliance with regional legislations and global regulations is crucial to stay clear of lawful risks. Each territory has particular needs relating to firm enrollment, reporting, and taxation, which should be extensively researched.

Business owners should acquaint themselves with the policies controling corporate framework, ownership, and operational practices in the chosen offshore place. In addition, anti-money laundering (AML) and understand your customer (KYC) laws usually apply, needing proper documents and verification processes.

Engaging with legal specialists who this content concentrate on overseas solutions can give important guidance on maneuvering with these intricacies. Guaranteeing conformity not just protects the company from possible lawful issues however also improves credibility with regulators, investors, and companions. By sticking to the proposed lawful structures, business owners can efficiently take advantage of the advantages of overseas firm formations while minimizing risks related to non-compliance.

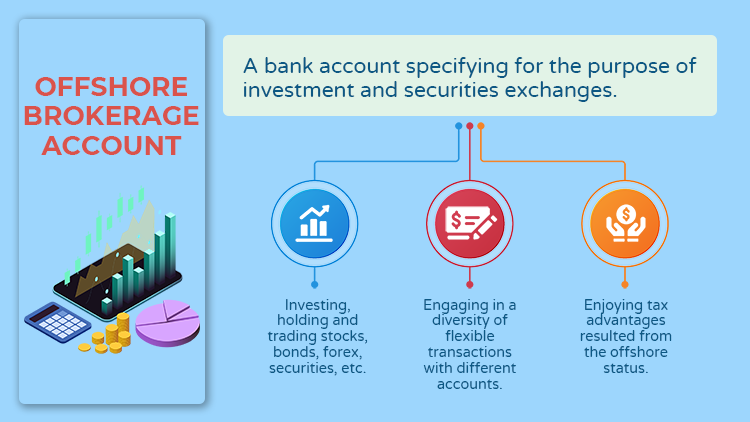

Establishing Up Financial and Financial Accounts

As soon as an appropriate financial institution is recognized, business owners usually require to prepare and submit numerous documents, consisting of evidence of identification, organization enrollment files, and a description of the designated business tasks. (Offshore Company Formations)

Some financial institutions might additionally need a minimum deposit to open an account. Entrepreneurs need to be prepared to answer concerns relating to the resource of funds and company operations. By completely recognizing the financial landscape and following the bank's requirements, business owners can protect their overseas firm has seamless access to crucial economic solutions for reliable operation.

Preserving Your Offshore Business: Ongoing Obligations and Ideal Practices

Maintaining an offshore firm entails a number of ongoing duties that are important for compliance and operational honesty. Trick elements consist of sticking to annual conformity demands, maintaining precise financial documents, and understanding tax commitments. These components are essential for making certain the company's durability and legal standing in its territory.

Yearly Conformity Requirements

While developing an offshore company provides various advantages, it additionally requires ongoing duties that can not be forgotten. Yearly compliance needs differ by jurisdiction but usually consist of sending financial declarations and yearly returns to regional authorities. Companies must additionally pay annual costs, which can consist of registration revivals and taxes, depending upon the place. Additionally, numerous territories require maintaining a licensed office and a neighborhood representative. Failure to abide by these guidelines can lead to fines, including penalties or also dissolution of the business. Entrepreneurs need to also be conscious of any kind of modifications in neighborhood laws that may impact their compliance responsibilities. Remaining notified and arranged is necessary for maintaining the benefits of an overseas firm while meeting legal obligations properly.

Keeping Financial Records

Conformity with yearly needs is just part of the continuous obligations linked with offshore firm management. Preserving accurate monetary documents is essential for assuring transparency and responsibility. Business owners have to methodically record all purchases, consisting of revenue, expenditures, and assets. This method not only aids in inner decision-making however likewise prepares the business for prospective audits from governing authorities.

Regularly updating economic declarations, such as earnings and loss accounts and annual report, is crucial for tracking the firm's economic wellness. Utilizing bookkeeping software application can enhance this procedure, making it less complicated to keep and generate records conformity. In enhancement, business owners should consider looking for expert accounting services to assure adherence to regional policies and ideal practices, therefore securing the stability and credibility of their offshore procedures.

Tax Obligations Review

Steering via the complexities of tax commitments is vital for the effective monitoring of an offshore firm. Entrepreneurs should comprehend the tax obligation policies of both their home nation and the territory where the offshore entity is developed. Compliance with neighborhood taxes legislations is vital, as failure to have a peek here stick can lead to fines or lawful concerns. Regularly filing essential income tax return, even when no tax obligation might be owed, is often review required. Additionally, keeping accurate and updated financial records is essential for showing compliance. Consulting from tax experts acquainted with worldwide tax obligation regulation can help browse these obligations successfully. By applying best techniques, business owners can guarantee that their offshore procedures stay monetarily viable and legally compliant.

Regularly Asked Inquiries

The length of time Does the Offshore Firm Formation Refine Typically Take?

The overseas company development procedure commonly ranges from a few days to several weeks. Aspects influencing the timeline consist of jurisdiction, paperwork requirements, and responsiveness of financial and legal organizations associated with the setup.

What Are the Prices Related To Maintaining an Offshore Business?

The prices connected with keeping an offshore firm can vary commonly. They commonly consist of annual enrollment costs, conformity costs, accounting solutions, and feasible legal charges, depending on the jurisdiction and certain company activities included.

Can I Open a Personal Savings Account for My Offshore Company?

Opening an individual savings account for an offshore firm is generally not permitted. Offshore accounts should be business accounts, showing the business's tasks, therefore conforming with guidelines and ensuring proper financial administration and lawful accountability.

Exist Constraints on Foreign Ownership of Offshore Firms?

What Happens if I Fail to Abide By Offshore Rules?

Failing to abide by overseas guidelines can bring about severe penalties, consisting of substantial penalties, loss of organization licenses, and possible criminal charges. Furthermore, non-compliance might lead to reputational damages and difficulties in future service procedures.

Offshore companies are entities signed up outside the individual's country of home, frequently in jurisdictions that supply beneficial regulative atmospheres. Selecting the ideal jurisdiction for an offshore company is vital for making best use of tax advantages and making certain compliance with local guidelines. When taking into consideration the facility of an overseas company, recognizing the tax obligation advantages linked with numerous jurisdictions is crucial. Picking the appropriate territory for an offshore firm calls for a thorough understanding of the regulatory atmosphere, as different countries impose varying levels of compliance and administration. In addition, the political security and credibility of a territory can affect the long-lasting feasibility of the offshore firm.